Second Act

On any given Wednesday at 3 a.m., almost two hours before the sun will rise, John Paider finishes his 12-hour shift at A to Z Machine Company Inc., an employee-owned machine shop in Appleton. While the average age of his second-shift coworkers stands at 31, Paider is 73. Not only is he the oldest member of the second-shift team, he’s also the oldest employee of the entire company. Although working the night shift and more than 40 hours a week may not be a goal — or even physically possible — for most people his age, this is how Paider likes to stay busy.

Paider, part of the baby-boom generation born between 1946 and 1964, grew up on his family’s dairy farm in Denmark, Wisconsin, south of Green Bay. He developed his work ethic when he was about 3, when he was assigned the job of feeding his family’s cows.

About 59 years later, in 2008, Paider retired from his full-time job at a machine shop. He continued his childhood passion and helped out on local crop farms, but the job’s hours were sporadic.

John Paider returned to a career in machining after initially deciding to retire. (Photo by Lily Oberstein)

About two years later, he received a phone call from A to Z Machine. Paider’s son-in-law — who was fixing a copier in the company’s office — had mentioned to a company partner that Paider, who was bored at home, needed a job to stay busy. Although he had no real financial reason to return to the labor force and taking the job meant driving 61 miles every day he worked, Paider jumped at the opportunity.

He restarted his machining career at 64 years old, and even on his first day at A to Z Machine after a two-year machining hiatus, Paider was anything but nervous.

He was excited.

“I always tell [my boss], as long as I’m healthy and able to do my job, I say, ‘Please let me work,’” Paider says.

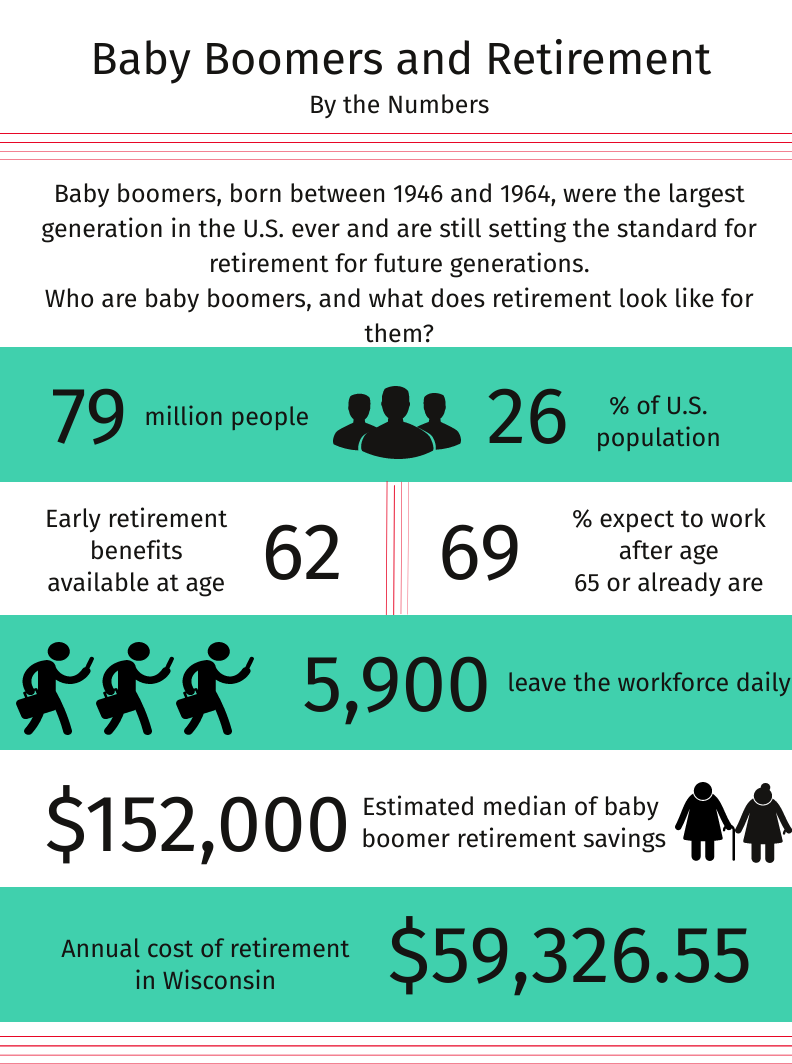

According to the National Association of Social Insurance the age to collect full Social Security retirement benefits is 66. However, the Pew Research Center reports that baby boomers are choosing to stay in the workforce longer. In 2017, 19.1 percent of eligible Wisconsin retirees were still working — nearly a 5 percent increase since 2000, according to the UW-Extension Center for Community and Economic Development.

Retirement can be a vast unknown. Some have to budget for more than 30 years, depending on when they choose to retire; others decide to continue to work out of necessity or personal choice; and some retire and then re-enter the workforce just a few years later. Whatever their reasons, as Wisconsin’s baby boomers move through their retirement years, they are altering how retirement could look for future generations.

According to Crystal Carlson, a senior financial adviser at Merrill Lynch Wealth Management in Madison, financial planning — the backbone of outlining and preparing for retirement — has changed. A decade ago, adults who were thinking about retirement started to speak with financial planners in their late 30s or early 40s. Now, the standard is shifting, and clients are beginning to work with a financial planner in their early 20s — or as soon as they start their careers. Carlson attributes this change in mindset to the parents of these young adults, who are serving as examples to their children for why they should start planning earlier in life.

“[They] will start asking about, ‘OK, how much should I save? What’s the best way to save?’ because I think there is a lot more awareness about the long-term detrimental side effects of not saving, so we see it a lot earlier,” Carlson says.

After working for more than 30 years, Susan Lampert Smith recently announced her early retirement.

Susan Lampert Smith also had some financial considerations before she announced her retirement fall 2019. Lampert Smith, 60, is a media relations strategist for UW Health and the University of Wisconsin Carbone Cancer Center and a senior lecturer at UW-Madison. She has worked two jobs throughout most of her adult life and credits both for her ability to retire at a younger age.

Although Lampert Smith’s financial planner originally advised her to retire at 62 because of her finances, she was able to push up her end date by rebalancing her monthly budget for when she did retire.

“Start early if you can, because you don’t think you’ll get old, but you will,” Lampert Smith says.

While many people such as Lampert Smith hope to retire early, others forgo their retirement plans completely to continue their careers. Steve Walters, 72, chose not to retire from his career as a journalist out of passion for the state’s political climate. He instead opted to continue working part time as a senior producer for WisconsinEye, a public affairs cable network in Madison.

Twelve years ago, Walters’ friends met with a financial planner and were told they would need to save $1 million to retire comfortably. Although Walters was shocked by the sum, it served as a wake-up call.

“We aggressively saved and paid off everything like five years ago, so we are debt-free, which means I don’t have to work,” Walters says of his shared finances with his wife.

Because his paychecks aren’t needed to support his family, Walters will use his extra income this upcoming year to pay for things such as vacations and two new roofs — one for his house and one for his cottage.

But for those on the cusp of retirement, continuing to work is not always for personal fulfillment. With common financial setbacks, such as divorce or sickness, funding retirement isn’t easy. According to the Associated Press-NORC Center for Public Affairs Research, 32 percent of adults who are 50 years or older do not think they will be prepared when the time to retire comes.

Carlson says that while older generations and some of the early baby boomers could rely on pensions, the majority of retirement costs fall on the shoulders of the retiree, increasing the importance of the retirement plans companies offer.

She recommends her clients replace 75 percent of their full-time income in retirement. If her clients’ retirement fund falls short of their retirement savings goal, the options are to either save more or work longer.

For Lampert Smith, striking a balance between having enough money to see herself through retirement, as well as enjoying her life while still healthy, was one of the biggest considerations in her choice to retire.

She had talked with a friend about what the two would do after they retired — but shortly after her friend reached that milestone, she fell ill and passed away. This caught Lampert Smith’s attention.

“You know on one hand, we think we’re going to be retired for 30 years, but you don’t know how much time you have. The time that you have that you’re in good health or you can actually do fun things is short, so I decided to maximize mine,” Lampert Smith says.

Paider’s thoughts on retirement are different, however. He thinks that not working will have negative effects on his health. He says many of his retired friends who haven’t continued working on other projects look older and are in worse health than he is.

Instead of drawing up a retirement plan, he jokes he’ll quit working only when he can collect his life insurance policy.

Walters isn’t as worried about staying busy after he retires, though. Already an active volunteer in his community, he would simply spend more time serving at his church.

But he won’t step away from his job quite yet. “How can one retire looking at the next fascinating election year?” he says.

Still, Walters’ future holds a lot of personal unknowns. “Will I still be healthy, will I still be interested, will I still find the process and the people and the public policy interesting?” he asks.

Lampert Smith does not intend to make plans for her first year of retirement besides traveling and spending more time with her family. While the ambiguity of retirement can be scary for some, Lampert Smith is excited to transition out of the workforce, saying that the experience reminds her of the thrill of her youth.

“Remember when you were in high school and you knew you were going to college, but you really didn’t know what college was?” she recalls. “That’s kind of where I’m at right now. It’s like, you know there’s going to be this different world, but you don’t really know what it is.A

Ally Melby | Managing Editor

Senior studying strategic communication and reporting with a digital studies certificate