also in practical:

about

advertise

subscribe

contact

site

map

| advertisement |

|

Debt, page 2

by jason soriano

At first, Manson splurged. She bought a new digital camera and “updated her business wardrobe” to keep up with the rest of the corporate world. Thankfully, Manson reigned in her spending habits when she decided to put a large chunk of her paycheck toward the purchase of a condominium.

“I never had a choice,” Manson says. “I refused to carry a balance on my credit cards, and I couldn’t afford to spend any more.”

While Manson’s conservative attitude prevented her from living beyond her means, Schmick and Traubenberg were not as fortunate. Between going out with friends, furnishing their apartment and paying for car repairs, the couple racked up large debts they were unable to pay off immediately.

Schmick also observed many of his fellow programmers spending money they didn’t have. “Some of my friends who said over and over how broke they were would just randomly spend hundreds of dollars on a new [computer] program,” he says.

Kathryn Crumpton, general manager of Consumer Credit Counseling Service of Greater Milwaukee (CCCS), has many clients with similar stories.

“A lot of students have this ‘I deserve it’ attitude once they graduate,” Crumpton says. “A lot of them expect to get that great salary right out of college, but they’re really making squat starting out.”

Seventh Level of Plastic Hell

Intelligent, hardworking consumers like Schmick and Traubenberg perhaps should have realized earlier that their spending outpaced their salaries. But they are not completely to blame for living beyond their means. After all, money never really changed hands.

At first the pair paid their bills with money from their salaries. Then other bills arrived. Car payments, insurance bills, textbook bills and even “good” debts like student loans accumulated. When this became too much to handle with their paychecks alone, Traubenberg paid off the remainder with a credit card. When one card maxed out, she signed up for another. By the time Traubenberg realized how bad her finances were, she had seven credit cards.

A recent study by student loan provider Nellie Mae found that on average, 56 percent of all graduates carry at least four credit cards and an average balance totaling $2,864. Financial experts agree that short-term solutions like credit cards are one of the best ways to permanently fall into a habit of overspending.

“Kids see a credit card and go, ‘Free money! Let’s go party!’” Crumpton says. “It’s a great way to end up in credit card hell.”

But the money isn’t free. Hidden fees, high interest rates and the infamous “fine print” are all ways credit card companies make money. And often buyers never realize how much money they spend because a cash transaction never takes place. For many, it never even registers that they buy too much. Traubenberg thought she was being responsible when she paid the minimum monthly balance on their credit cards each month, but she lost ground as interest accumulated. Estock asserts that on average, a credit card purchase costs the buyer 112 percent more than the original purchase itself.

“Most people are surprised to find that even ‘cheap’ purchases for something like a $30 sweater suddenly become $80 over time when credit card interest sets in,” Estock says. And as purchases compound, many spenders use the majority of their paychecks to simply break even.

A snowball effect

Some young professionals knowingly live beyond their means and make no attempt to reconcile debts. Underestimating the repercussions of poor spending habits is as bad as the habits themselves. Everyone knows an unpaid water bill results in the water being shut off. Consequently, some young professionals assume that, at worst, banks and credit card companies simply take back those items for which you didn’t pay.

<- previous page |back to top | next page ->

|

||||

|---|---|---|---|---|

|

||||

financial failure: Young professionals often spend money they don't have. photo: derek montgomery |

||||

quiz: financial pitfalls |

||||

|

||||

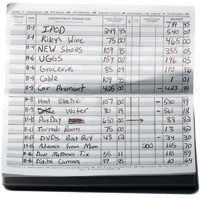

what to avoid: An overdraft charge is only the first consequence of not being financially balanced. photo: derek montgomery |

||||

home

| professional

| recreational

| practical

| social

about | advertise

| subscribe

| contact

| site

map

curb magazine 2005: balance for wisconsin's young professionals