also in practical:

about

advertise

subscribe

contact

site

map

| advertisement |

|

Debt, page 3

by jason soriano

Sadly, this is a naive assumption. Legal actions like repossessions or wage garnishments are only the beginning of how living beyond one’s means can hurt in the long run. Once bad debt accumulates, the results can snowball into major life roadblocks. While a single missed credit card payment might not cause much damage, financial institutions will label consumers as bad credit risks if they repeatedly miss payments or default on loans. This is when the situation gets ugly. The effects of damaged or bad credit ripple throughout life.

Bad credit means most lenders are unwilling to invest in a person again. While credit card companies are more than happy to send bankrupt consumers dozens of new credit card offers, financial institutions like banks are not as forgiving. “Future loan applications for things like houses or cars can be denied because of bad credit,” Estock says. And those willing to lend money to someone with bad credit often do so at a higher interest rate, which drives many further into debt. Crumpton says even a new job might be out of the question. “A lot of employers look at credit scores when you are being interviewed for a job,” Crumpton says. “How do you expect to get that dream job if no one will hire you?”

Reversing Trends

Fortunately, Traubenberg and Schmick’s financial situation never completely deteriorated. Since her father was in the banking business, Traubenberg knew how to rescue a bad financial situation. “We cut down the number of credit cards we had and wrote down the budget for everything,” Traubenberg says. At the same time, Schmick increased the monthly payments on the credit card debts, which cut back on their accumulated interest.

“There is a lot more to managing money than just paying the bills,” Schmick says. “You need a lot of focus.”

But unlike Schmick and Traubenberg, many young professionals lack the skills to manage their own debt, and families are often inadvertently the source, not the solution, of financial mismanagement.

“If no one warns their kids about the dangers of overspending, and if they themselves have bad habits, kids aren’t going to learn the [financial] skills they need,” Crumpton says. Crumpton says she often counsels entire families who have passed on their bad habits to their children.

Fortunately, groups like the CCCS and the UW Credit Union are happy to help young professionals get their finances on track. CCCS organizations around Wisconsin hold monthly financial management seminars, and the UW Credit Union offers numerous online self-help guides. But Crumpton stresses that the ability to manage money does not come quickly.

“Money management is a skill,” Crumpton says. “You have to learn it to be good at it.”

Looking to the future

When people do learn the skills, the rewards can be great. With a much smaller debt load and now only two major credit cards, Schmick and Traubenberg were able to look beyond their finances and focus on one another. They married in 2004 and recently put a down payment on a new home in Madison. Schmick now handles numerous jobs for large Madison companies and specializes as a digital technician and web designer; Traubenberg will graduate this semester as a fully registered nurse.

While Schmick and Traubenberg’s story has an optimistic outlook, others are not as fortunate. In 2001, the average 25-to 34-year-old spent nearly 25 cents of every dollar of income on debt payments and had the second-highest rate of bankruptcy in the United States. Estock says that without careful planning, good financial management and personal discipline, young professionals will continue to live outside of their means with disastrous results. “The light at the end of the tunnel is there,” Estock says. “But you have to know when you’re in trouble and you have to ask for help.”

|

||||

|---|---|---|---|---|

|

||||

financial failure: Young professionals often spend money they don't have. photo: derek montgomery |

||||

quiz: financial pitfalls |

||||

|

||||

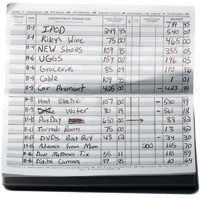

what to avoid: An overdraft charge is only the first consequence of not being financially balanced. photo: derek montgomery |

||||

home

| professional

| recreational

| practical

| social

about | advertise

| subscribe

| contact

| site

map

curb magazine 2005: balance for wisconsin's young professionals